Sovereign financial infrastructure partnership model

Creating a national financial asset through strategic partnership.

Every country is different. Each engagement is tailored to the country's economic priorities, regulatory framework and long-term objectives. What follows describes the general structure of a typical partnership.

What is established

The outcome of a sovereign partnership is the establishment of a locally incorporated enterprise, jointly owned by the host country and PayServices, operating under the laws, regulatory framework and institutional requirements of the host nation.

The enterprise carries the ITAM brand alongside the national identity of the country, reflecting both the partnership and its sovereign character. It represents a locally established financial infrastructure company designed to strengthen national financial capability while connecting the country to a broader global financial ecosystem.

This enterprise becomes the operator of the country's financial hub, providing the foundational infrastructure required for secure, transparent and efficient financial activity. The platform includes:

- A modern banking infrastructure

- National clearing and settlement capabilities

- Integrated compliance and risk management frameworks

- Secure domestic and cross-border payment connectivity

- Connection to the broader PayServices network and verified counterparties

Through this structure, the country gains a modern financial operating platform capable of supporting government institutions, financial institutions, businesses and citizens.

The host country is not purchasing a system, outsourcing its financial infrastructure, or imposing a new fee or charge on citizens or financial institutions.

Instead, the country becomes an equity partner in the locally incorporated enterprise that owns and operates the financial infrastructure. As a shareholder, the country participates in the long-term value created by the enterprise, aligning national interests with the growth, success and sustainability of the financial hub.

The partnership model creates shared incentives:

- The country benefits as the platform expands and generates economic value.

- PayServices benefits through the successful operation and scaling of the enterprise.

- Financial institutions benefit from improved infrastructure, compliance capabilities and connectivity.

The objective is to create a national financial asset, not simply to deploy technology.

Governance and ownership

The enterprise operates through a shared governance model with representation from both the host country and PayServices. A joint board of directors is established to ensure:

- Strategic alignment between the parties

- Protection of national interests

- Operational accountability

- Long-term sustainability

A chairman is selected through the agreed governance process, ensuring balanced leadership and alignment between the host nation and PayServices.

The structure respects the sovereignty of the host country while providing access to the technology, expertise and global financial connectivity required to operate a next-generation financial ecosystem.

How an engagement proceeds

The process is shaped by the host government and its institutions. The following represents the typical framework.

Introduction at head of state level

The initiative is introduced to the head of state, head of government, or an appropriate senior government office. The initial discussion focuses on the national opportunity:

- Strengthening financial sovereignty

- Modernizing financial infrastructure

- Improving transparency and compliance

- Expanding economic participation

- Enhancing national security capabilities

The introduction is typically facilitated through an official channel, trusted advisor or qualified business representative.

Presentation to finance ministry and central bank

Following initial government interest, the initiative is presented to the institutions responsible for financial policy and oversight. These may include:

- Ministry of Finance

- Central bank

- Treasury authorities

- National banking associations

- State-owned financial institutions

This engagement is intentionally multi-institutional, ensuring that the organizations responsible for operating and regulating the financial system participate from the beginning.

Agreement

Once institutional alignment is achieved, the parties execute a formal agreement. The signing entity varies depending on the country's legal structure and government direction. In some jurisdictions this may be:

- Ministry of Finance

- Central bank

- State-owned financial institution

- Another government-designated entity

The structure is determined by the host government, and the process is documented through each stage.

Formation of the joint enterprise

The enterprise is incorporated locally and jointly owned by the parties. Depending on local requirements, a portion of ownership may be reserved for qualified local participants, including strategic partners, business organizations and contributors who support the establishment of the enterprise. Ownership interests may be represented through a local holding structure.

A board of directors is established, and governance begins in accordance with the agreed partnership framework.

Deployment and operation

The platform is deployed, compliance standards are implemented, and the enterprise begins operating the financial hub. At this stage, the initiative transitions from a development project into an operating commercial enterprise.

What each party contributes

PayServices contributes

The host country contributes

Regulatory framework and legislation

In most jurisdictions, new legislation is generally not required. Governments typically already possess authority under existing financial, regulatory and national security frameworks to establish standards designed to protect the integrity of financial markets.

The adoption of a common compliance protocol generally operates within existing regulatory authority rather than requiring the creation of an entirely new legal framework.

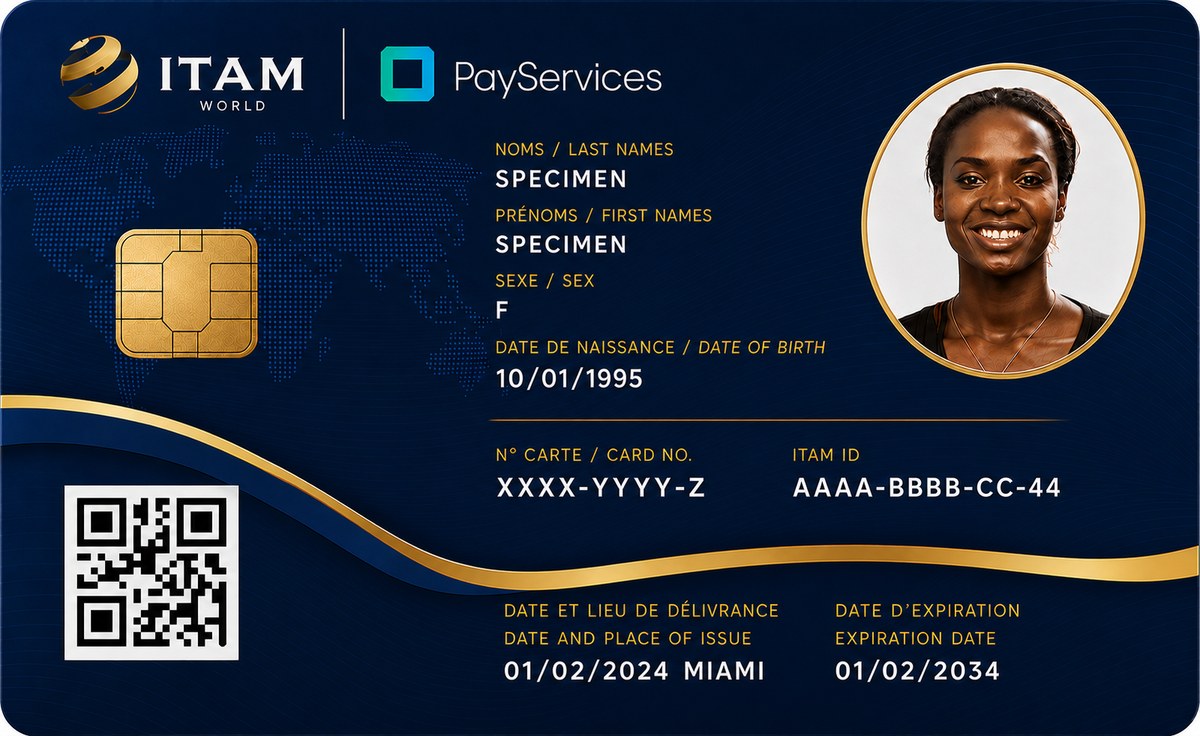

The credential — digital and physical

The hub is infrastructure; the credential is where citizens meet it. It rests on a single premise: one credential should be the only one a person needs — for their identity, their entitlements, their health services and their money.

The identity itself is digital. It is the ITAM ID, and it lives on the network, not in anything a citizen carries. What a citizen carries is a way to present it — and there are two.

The mobile application

The primary form. A citizen with a phone holds their identity, accounts, wallets and entitlements in an application, and presents them wherever the network reaches.

The card

For everyone else, and for everywhere else. No phone, no signal, no literacy requirement, no battery. The card works at a rural clinic and a remote border post exactly as it works in a capital city.

Both resolve to the same ITAM ID on the same hub. A citizen may hold one or both; the network does not distinguish between them, because neither of them is the identity. They are how the identity is presented.

This matters for how a national deployment is judged. A programme that depends on smartphone ownership excludes the people who most need including. A programme that issues only cards ignores the phones already in circulation. The credential exists in both forms so that reach is never a function of what a citizen happens to own.

The physical form: a specimen credential. One credential for identity, entitlements, health services and money — carrying an identifier, a name and a photograph, and nothing else. No account number, no keys, nothing that can authorize a transaction on its own.

The card is a passive token

The card carries no account number, no track data, and no private cryptographic keys. It cannot authorize a payment, sign a message or complete a transaction on its own. It is a set of identifiers and a sealed data container — nothing more.

The consequence is the point: a lost or stolen card conveys no usable capability to whoever finds it. There is nothing on it to clone, skim or replay. The fraud that card-present systems are built to survive simply has no surface to attack.

What it carries

The credential stores a unique identifier — the ITAM ID, an International Trusted Account Marker — together with the holder's name and photograph. It may also carry encrypted records for national identity, driver's licences, health entitlements or access rights, readable only by the authority entitled to them.

Two numbers appear on the card, and neither is an account number. The ITAM ID identifies the person: it persists for life, across every reissue, and it is what the network resolves to reach their accounts, wallets and entitlements. The card number identifies only the piece of plastic itself — the physical artifact, which changes whenever a card is replaced.

Neither number contains anything. The ITAM ID resolves to accounts, wallets and entitlements held on the hub; it does not hold them. The card number resolves to a card. The card points; the network holds.

The distinction is what makes a lost card unremarkable. The plastic is replaced and its number is retired; the person's identity, accounts and entitlements are untouched, because none of them were ever on the card.

Verification without connectivity

Because the photograph is stored on the card itself, an officer at a border post, a clinic or a checkpoint can verify the holder against the credential with no network connection at all. This matters in precisely the places where connectivity cannot be assumed and identity assurance matters most.

The only credential a person needs to carry

Most people carry a wallet full of documents: a national identity card, a driver's licence, a health card, a bank card or two, a transit pass, a badge for work. Each is issued by a different authority, each proves one thing, each is lost or stolen separately, and each has to be replaced on its own terms.

This replaces the wallet. One credential — on a phone, in a pocket, or both — gives its holder their identity, their entitlements and their money — not as a bundle of separate documents pressed into one piece of plastic, but because every one of those things is simply an entitlement linked to the same verified identity. The card proves who you are. What that entitles you to is a question the network answers.

At a clinic it is a health card. At a border post it is an identity document. At a merchant it is a payment instrument, and the holder chooses at the terminal which account or wallet to draw on. At a government office it is proof of entitlement. The credential itself does not change — it expresses no preference, because it knows nothing about any of them. What changes is the question being asked of the network.

For a citizen carrying one credential instead of six documents, this is convenience. For a government, it is the same identity verified consistently across every service the state provides — and for people who have never held a bank card or a formal identity document at all, it is a single step into both at once.

Where the intelligence lives

All routing, account selection, decryption and cryptographic work happens on the terminal and backend of the hub — the infrastructure the joint enterprise operates. The card is deliberately inert so that the intelligence sits where the country and PayServices jointly govern it.

This is why ownership of the hub matters. In a conventional card scheme the intelligence sits in the card and the scheme rules sit abroad. Here it sits in infrastructure the host nation co-owns.

Legacy environments

Where a terminal running the hub's software is not present, the printed code on the card resolves the same identity and service flow through a secure endpoint on any browser or mobile device. Deployment is not gated on replacing every terminal in the country first.

Why financial institutions participate

The adoption of a government-supported compliance standard reduces the burden placed on individual financial institutions. Rather than each institution independently developing, maintaining and defending separate compliance systems, participating institutions operate through a nationally recognized standard.

This approach:

- Reduces compliance complexity

- Lowers operational burden

- Improves transparency

- Strengthens risk management

- Creates consistency across the financial system

The network becomes an enabling infrastructure rather than an additional regulatory burden.

Data sovereignty

Control over financial data remains a decision of the host country. Where a government requires domestic data residency, a national data center can be established and operated within the country, ensuring that financial data remains hosted on national territory.

A national data center represents a significant infrastructure investment. Where a country determines that such investment is not immediately required, alternative arrangements may be considered, including:

- Existing PayServices infrastructure

- Approved regional hosting arrangements

- Other legally permitted infrastructure solutions

Regional hosting is ordinary practice in established markets — within Europe, for instance, a Belgian institution may host its data in France without difficulty, because the legal framework between those countries accommodates it.

The appropriate structure depends on:

- National law

- Security requirements

- Strategic priorities

- Investment objectives

Data sovereignty is addressed as part of the initial design process with each government.

Why countries establish the financial hub

National security and financial visibility

Operating this infrastructure provides the government with enhanced visibility into financial activity within its jurisdiction. Understanding financial flows, participants and transaction patterns supports:

- National security objectives

- Financial integrity

- Anti-financial-crime initiatives

- Market transparency

Financial inclusion

Where permitted by local law, the platform supports broader access to formal financial services. This may include the ability to provide current accounts without minimum fees to be opened and maintained, extending financial services to populations previously underserved by traditional banking infrastructure.

Financial inclusion becomes a fundamental component of national economic participation.

Revenue without taxation

The enterprise generates revenue through the financial services and infrastructure it provides. The country participates in this value creation as an equity partner.

This is not a tax, fee or government-imposed charge. The country earns through ownership in the company operating the financial infrastructure, and benefits as the enterprise grows.

Establishing regional financial leadership

A national financial hub positions the country as a regional financial center. The potential benefits include:

- Increased investment activity

- New employment opportunities

- Financial sector growth

- Economic diversification

- Greater participation in international commerce

The infrastructure itself is the foundation. The broader opportunity is what the infrastructure enables.

Beginning the conversation

Each partnership is designed around the unique circumstances of the country it serves, including:

- National laws

- Regulatory structure

- Existing financial infrastructure

- Economic priorities

- Strategic objectives

The detailed structure, roadmap, governance model and commercial terms are developed jointly with government counterparties.

Engagements with governments, central banks, finance ministries and state institutions are conducted through the formal channels of PayServices.

Boise, Idaho 83702-6140

United States